Between 2007 and 2024, UK car-finance lenders paid dealers commissions that were hidden from, or not properly disclosed to, the customer, often inflating the interest rate the customer paid. The Supreme Court ruled on the practice in August 2025. The FCA confirmed an industry-wide redress scheme in March 2026: roughly £7.5bn of compensation, £9.1bn of total cost to firms, 12.1 million eligible agreements.

Those are the numbers everyone reports. But the FCA’s totals are abstractions. The bill itself is landing somewhere concrete: in the statutory accounts each lender files at Companies House. We read them.

Across the 17 exposed lenders, combined profit before tax swung from +£156M to −£1.09bn in the latest filed year, a swing of −£1.25bn, with 13 of the 17 loss-making. The filings show who is taking the hit, how hard, and what it is doing to the market: one major lender is quitting UK consumer finance.

How we got here

| Date | Event |

|---|---|

| Apr 2007 – Nov 2024 | Period covered by the redress scheme |

| Jan 2021 | FCA bans discretionary commission arrangements (DCAs) |

| Jan 2024 | FCA opens review of historic DCA complaints; complaint-handling paused |

| Oct 2024 | Court of Appeal finds for consumers in Hopcraft / Wrench / Johnson; lenders begin provisioning in earnest |

| Aug 2025 | Supreme Court: dealers owe no fiduciary duty (lenders win on Hopcraft and Wrench), but Mr Johnson wins under s.140A Consumer Credit Act. His undisclosed commission was £1,650.95, over a quarter of the car’s price; the remedy was the full commission back, plus interest |

| Oct 2025 | FCA consults on a scheme then estimated at ~£11bn total cost |

| Mar 2026 | FCA final rules (PS26/3): ~£7.5bn redress, £9.1bn total cost to firms, 12.1M agreements, average payout £829. Around 90,000 Johnson-type consumers (contractual tie and/or a DCA plus very high commission) get the full commission back with interest |

| Apr–May 2026 | FirstRand, owner of MotoNovo, announces a UK exit, calling the scheme “deeply flawed”; four legal challenges are filed against the scheme; the FCA says it will defend it “robustly” |

| May 2026 | With the challenges before the courts (a hearing is not expected before October 2026), the FCA tells firms to keep preparing but stops holding them to the scheme’s customer-contact timetable |

| Jun–Aug 2026 | Implementation deadlines under the scheme as made: lenders were to contact past complainants within 3 months and all other eligible customers within 6. Effectively on hold pending the challenges |

| Aug 2027 | Final consumer opt-in date under the scheme as made. The FCA originally expected millions of claims settled in 2026; it now says payouts are unlikely to begin before 2027 |

The scheme is opt-in (the FCA assumes ~75% take-up), covers discretionary commission arrangements, “high commission” cases and exclusive contractual ties, and the average payout is £829. The ~90,000 consumers getting full commission back are the exception, not the rule.

The damage, lender by lender

What follows is from the latest two filed periods per lender, taken from public Companies House accounts and verified line-by-line against the filed PDFs. Several of the provision figures below appear nowhere in a press release; they sit in the notes to accounts that almost nobody reads. Entity accounts and group results differ; each row says which it is.

The epicentre: the banks’ motor-finance arms

| Lender | FY end | PBT, prior → latest | Confirmed provision |

|---|---|---|---|

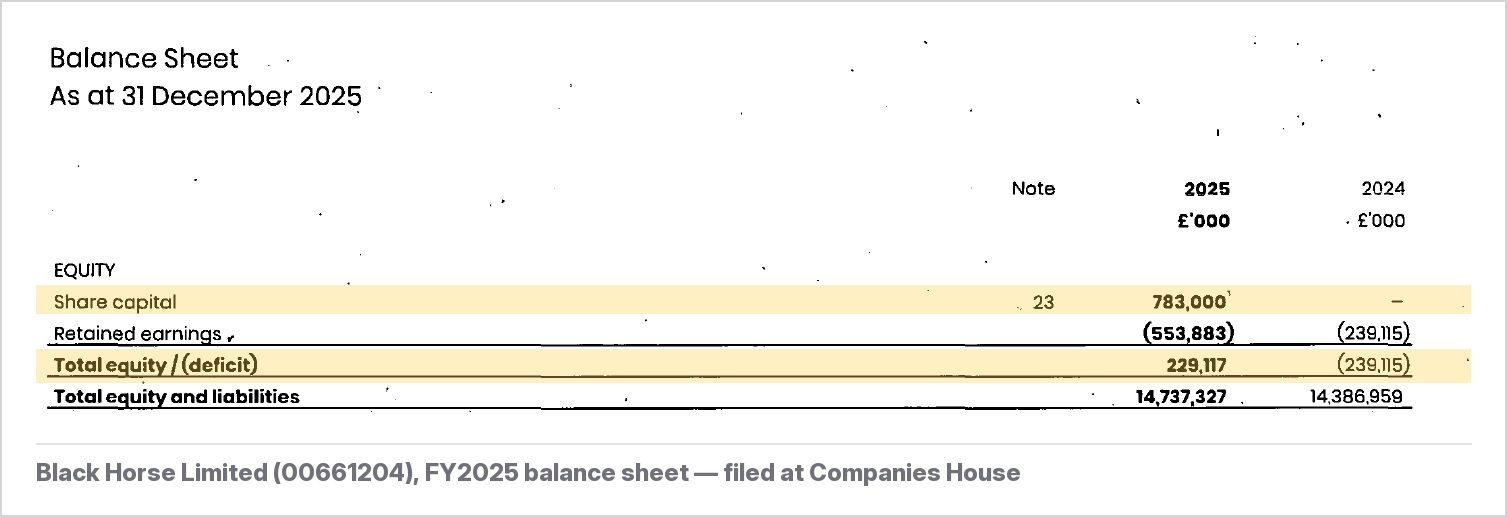

| Black Horse (Lloyds) | Dec 2025 | −£512M → −£418M | £1.95bn (Lloyds group) |

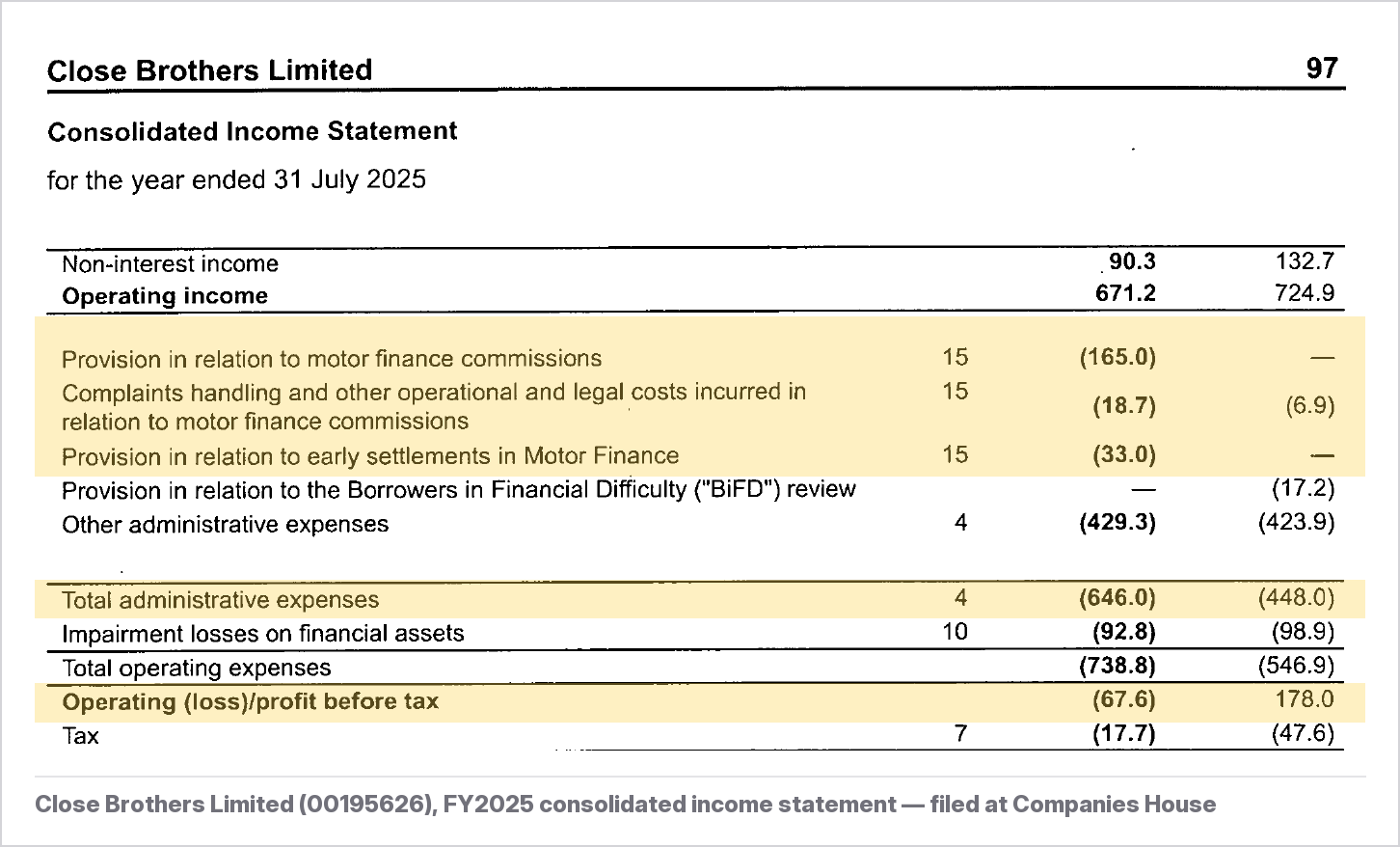

| Close Brothers Ltd (consolidated) | Jul 2025 | +£178M → −£68M | £165M + £33M remediation (FY25) |

| Santander Consumer (UK) | Dec 2025 | −£228M → −£125M | £461M (Santander UK) |

| MotoNovo Finance (FirstRand) | Jun 2025 | +£46.8M → −£24.6M | £750M (FirstRand group) |

| Clydesdale Financial Services (Barclays Partner Finance) | Dec 2024 | −£91.8M → −£162.2M | £325M (Barclays) |

Black Horse, the UK’s biggest car-finance provider, has now filed two consecutive heavy loss years, a cumulative −£930M. Close Brothers is the cleanest before-and-after in the dataset: a +£178M profit became a −£68M loss, with the accounts itemising a £165M commission provision, £33M of early-settlement remediation and £18.7M of complaints-handling costs inside a £198M admin-expense jump. It won its case at the Supreme Court and still swung to a loss. MotoNovo’s own accounts book a £58.5M commission provision, a fraction of FirstRand’s £750M group figure, for reasons we come to below. Barclays’ Clydesdale stopped writing motor finance in 2019, but the 2010–2019 book is in scope: an £88.4M “litigation and conduct” charge deepened its losses while total assets shrank from £2.6bn to £1.7bn. The book is being run down.

The manufacturer captives

| Lender | FY end | PBT, prior → latest | What the filed accounts disclose |

|---|---|---|---|

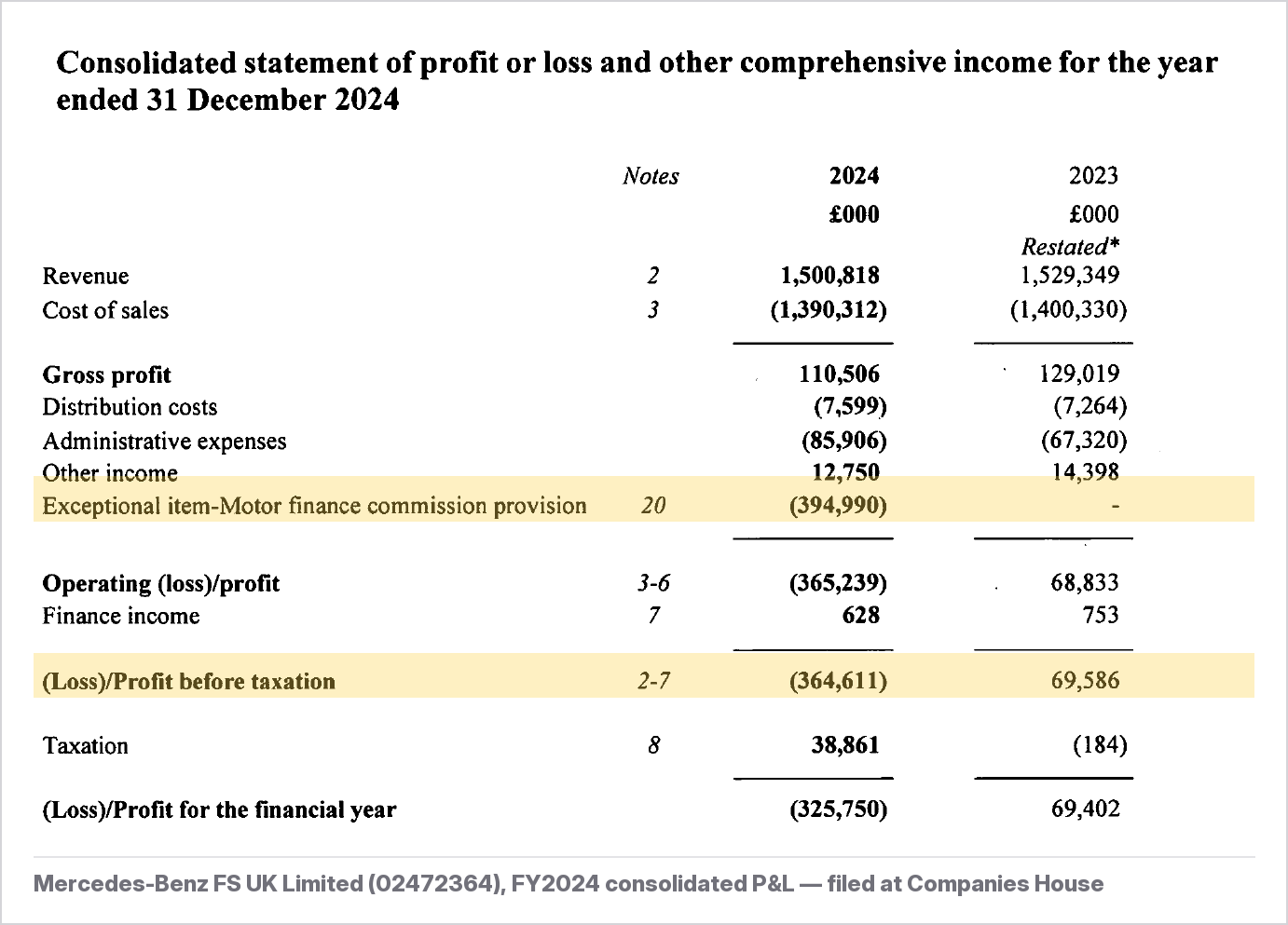

| Mercedes-Benz FS UK (consolidated) | Dec 2024 | +£69.6M → −£364.6M | A £395.0M “motor finance commission provision” booked as an exceptional item; now a legal challenger to the scheme |

| BMW FS (GB) | Dec 2024 | +£229M → +£39M | ”Historic commission claims” provision £70.3M → £206.9M; £150M dividend stopped |

| Volkswagen FS (UK) | Dec 2024 | +£374M → +£136M | No redress provision recognised: the accounts say no obligation can be reliably estimated; a legal challenger |

| Honda Finance Europe | Mar 2025 | +£14.1M → −£49.6M | A £62.2M “motor finance commissions” provision (2024: nil) |

| CA Auto Finance UK (Crédit Agricole) | Dec 2024 | +£21.3M → −£33.5M | A £131.5M gross redress provision (£70.4M net of a £61.1M third-party recovery asset); a legal challenger |

| RCI FS (Renault) | Dec 2024 | +£35.9M → +£4.6M | A £73.6M “legal & regulatory” provision (2023: nil) |

| Hyundai Capital UK (consolidated) | Dec 2024 | +£61.2M → +£36.0M | A £34.5M “customer remediation” provision (2023: nil); £100M dividend stopped |

Only two of those seven provision figures, BMW’s and Mercedes’, appear to have made the press. Honda’s £62.2M, CA Auto’s £131.5M, RCI’s £73.6M and Hyundai’s £34.5M sit in the notes to accounts filed at Companies House; we could find no press report of any of them. And Volkswagen FS is the outlier in the other direction: while every peer provisioned, it recognised nothing, stating that no obligation can be reliably estimated, and joined the legal challenge instead.

A caution that still matters: captive-lender results in 2024 can also carry credit impairments and electric-vehicle residual-value writedowns, so the provision is not necessarily the whole of any one swing. Mercedes’ loss in particular likely includes residual-value pain alongside the confirmed £395M.

The thin end: specialist and subprime lenders

| Lender | FY end | PBT, prior → latest | Note |

|---|---|---|---|

| Blue Motor Finance (consolidated) | Dec 2024 | −£10.6M → −£31.0M | The loss nearly equals its £31M of net assets |

| Startline Motor Finance (consolidated) | Dec 2024 | −£0.7M → −£16.8M | A £28.2M motor-finance-commissions provision; net assets £64M → £50M; dividend stopped |

| Moneybarn No.1 (Vanquis) | Dec 2025 | −£34.3M → −£12.9M | Two loss years; the parent bank is profitable; motor is the bleeding arm |

| Specialist Motor Finance | Dec 2024 | +£2.8M → −£1.9M | Net assets down a quarter |

| Billing Finance | Oct 2024 | +£0.6M → −£1.9M | A Northampton family-scale lender, loss-making in the same provisioning window |

The control group

| Lender | FY end | PBT, prior → latest |

|---|---|---|

| Toyota FS (UK) (consolidated) | Mar 2025 | +£148.9M → +£196.5M |

| FCE Bank (Ford Credit, consolidated) | Dec 2025 | +£117M → +£167M |

| Stellantis FS UK | Dec 2024 | net +£30.7M → +£50.5M |

| Advantage Finance (S&U) | Feb 2026 | +£16.5M → +£23.4M |

Same market, same years, same macro — profits up, dividends maintained (Toyota paid £78.6M, FCE Bank £500M). Car finance did not suddenly become a bad business; the visible differentiator is the size of each lender’s historic commission exposure and when it chose to book it. (These lenders are still in scope of the scheme like everyone else; their filed years simply absorbed it.)

Six things only the filings show

1. Black Horse traded with negative equity. At end-2024 its equity was −£239M. In October 2025 Lloyds quietly recapitalised it with a £783M share issue (it’s in the statement of changes in equity), restoring the balance sheet to +£229M. A solvent group, but the subsidiary’s accounts show the scandal physically blew through its capital.

2. Close Brothers’ scandal costs are itemised in its cost line. Admin expenses rose £448M → £646M, and the accounts name the parts: a £165M commission provision, £33M of early-settlement remediation and £18.7M of complaints-handling costs.

3. MotoNovo’s entity accounts hide the iceberg. The Companies House entity (incorporated 2018) shows a −£24.6M loss and a £58.5M commission provision; the historic 2007–2019 book (the bulk of FirstRand’s £750M group provision) sits on a London branch of a South African bank that files no UK statutory accounts. Entity-level data needs group context.

4. Dividends are the early-warning light. Santander Consumer (£70M → 0), BMW FS (£150M → 0), Hyundai Capital (£100M → 0) and Startline (£10.9M → 0) all stopped paying their parents the year they provisioned. Toyota and Ford kept paying.

5. Barclays is running its book down. Clydesdale’s total assets fell £2.6bn → £1.7bn while losses deepened: exit by attrition, a decade after it stopped writing new motor loans.

6. The losses reach the bottom of the market. Billing Finance, with £21M of turnover and about 110 staff in Northampton, swung to a loss in the same filing season as Lloyds. The same window, four orders of magnitude apart.

What happens next

- Exit. FirstRand is selling Aldermore and MotoNovo and leaving UK consumer finance: the first whole-market casualty, explicitly blamed on a scheme it calls “deeply flawed, disproportionate and unfair”. Someone has to buy a £4.4bn loan book mid-scheme.

- Litigation. Four challenges to the scheme are live: Mercedes-Benz FS, Volkswagen FS, CA Auto Finance, and Consumer Voice, the last arguing it under-compensates. A successful challenge moves every number above, and the timetable is already slipping: the FCA says payouts it expected to start in 2026 are now unlikely before 2027.

- Capital strain at the thin end. Blue Motor’s loss nearly equals its equity; Startline lost a fifth of its equity in a year. Consolidation (or failures) among subprime motor lenders is a live watch-item.

- Another wave is coming. Ten of the lenders above have December 2024 year-ends, filed before the Supreme Court ruling and the final rules. Their next accounts, filed through late 2026, will carry the top-ups. The filed losses to date (~£1.3bn in the latest year across this set) are a fraction of the FCA’s £9.1bn for a reason: provisions phase in over multiple filing years.

If you bought a car on finance

The FCA estimates 12.1 million agreements written between April 2007 and November 2024 are eligible. The scheme is opt-in and free, with no claims-management firm needed, and the average payout is £829, with a small minority of high-commission cases receiving substantially more.

One caveat on timing: the lenders’ legal challenges have put the timetable on hold. Under the scheme as made, lenders had to contact eligible customers during 2026, with a final opt-in date of 31 August 2027. The FCA has since said it will not hold lenders to those contact deadlines while the case is live, and that payouts are unlikely to begin before 2027. Nothing about eligibility changes; the dates will.

Methodology and fact-check ledger

All filed figures (profit before tax, equity, dividends, admin expenses, headcount, total assets) come from the statutory accounts each lender files at Companies House, and every figure quoted above was verified against the filed accounts PDF (statement page, note number and all) on 12 June 2026. Where a company files consolidated accounts the table says so; provisions held at group level (Lloyds, Santander UK, FirstRand, Barclays) are labelled as group figures. Regulatory and press-reported claims were checked against the sources below on 12 June 2026.

| Claim | Source |

|---|---|

| Final scheme: £7.5bn redress, £9.1bn total cost, 12.1M agreements, £829 average, opt-in, payouts from 2026 | FCA statement and PS26/3, 30 Mar 2026 |

| Supreme Court: no fiduciary duty; Johnson wins on s.140A | Judgment, 1 Aug 2025 |

| Lloyds provision £1.95bn, held after final rules | PA via Yahoo Finance |

| Close Brothers £165M + £33M provisions; group FY25 loss −£122.4M | CBG 2025 preliminary results |

| Santander UK provision £461M | Car Dealer |

| FirstRand £750M provision; UK exit | AM Online, Motor Trader |

| BMW FS provision £70.3M → £206.9M | Motor Trader, Car Dealer |

| Mercedes-Benz FS UK loss attributed to provision | BM Magazine |

| Barclays/Clydesdale provision £90M → £325M | Yahoo Finance |

| Four legal challenges; FCA defending | Motor Trader, Law Gazette |

| Timetable on hold during the challenges; hearing not before Oct 2026; payouts unlikely before 2027 | FCA statement, 8 May 2026, Motor Trader, 10 Jun 2026 |

| Filed provisions: Mercedes £395.0M (Note 20), BMW £206.9M (Note 18), Honda £62.2M (Note 27), CA Auto £131.5M gross (Note 16), RCI £73.6M (Note 22), Hyundai £34.5M (Note 25), Startline £28.2M, MotoNovo entity £58.5M; Black Horse £783M share issue; VW FS nil provision | Companies House filed accounts for each entity, verified 12 Jun 2026 |

This is analysis of public filings, not financial advice. Figures are stated as filed at the entity named; group provisions are labelled as group figures.